By Tim Houghten

In the words of the great Bob Dylan: the times “they are a-changin,” for Sean Morsi and Ajay Mehra — CEO and CFO of MOR Financial, respectively — the notion of shaking things up has been woven into their company’s genetic code. It may come as a surprise to hear that an asset- based lender, known for utilizing cutting-edge marketing and high-tech analytics, assert for a traditional approach in customer service and building lifelong client partnerships.

With an average yield returning 10.5% for their lenders, Morsi and Mehra have compiled more than $70 million in committed capital from their investors, with roughly $35 million in their active in-house servicing portfolio. Built in a relatively short period of time with a focus in Southern California, where both were raised, the two have also set their sites on penetrating the Florida, Nevada and Arizona markets.

Ajay came on board as a partner in MOR Financial in 2009, with both partners coming from established lending backgrounds before re-shifting focus after the market crash. “Since then, we’ve grown into a premier private lender here in Southern California, specifically around Los Angeles County,” notes Morsi.

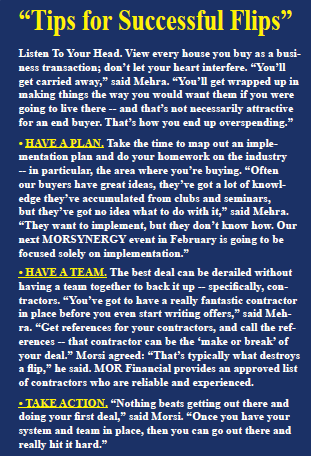

As the new kids on the block, the business moguls captured a very large percentage of the market in a very short span of time. A large percentage of their competition has been in the private money lending sector for 20 years or more. Mehra added that the industry had always been something of an “intuitive-based” one, which both men felt kept it from growing like it could. “We wanted to deliver structure,” said Mehra. “We wanted to shift the industry from the whimsicality it had.”

As the new kids on the block, the business moguls captured a very large percentage of the market in a very short span of time. A large percentage of their competition has been in the private money lending sector for 20 years or more. Mehra added that the industry had always been something of an “intuitive-based” one, which both men felt kept it from growing like it could. “We wanted to deliver structure,” said Mehra. “We wanted to shift the industry from the whimsicality it had.”

The demographic for private money investors today, according to the executives includes much of the younger mindset than was seen 10 or 15 years ago. The change in development is spawned mainly from disappointed and lack of confidence with the stock market and the desire for more tangible investments.

“Thanks to the stock market crash, several savvy financiers have a sour taste in their mouths, yet are still hungry for yield,” said Mehra. “We are seeing people, who would otherwise have investment portfolios centered around Wall Street now, deviating into real estate.” Today, instead of owning Microsoft as a growth stock, youthful investors would rather invest in assets they can hedge. The emerging generation with access to capital doesn’t have faith in the stock’s paper and would rather place funds into something concrete. At the end of the day, a hard asset like real property is never worth zero. They can hang their hat on that!

“Thanks to the stock market crash, several savvy financiers have a sour taste in their mouths, yet are still hungry for yield,” said Mehra. “We are seeing people, who would otherwise have investment portfolios centered around Wall Street now, deviating into real estate.” Today, instead of owning Microsoft as a growth stock, youthful investors would rather invest in assets they can hedge. The emerging generation with access to capital doesn’t have faith in the stock’s paper and would rather place funds into something concrete. At the end of the day, a hard asset like real property is never worth zero. They can hang their hat on that!

Another way the industry looks different today is the high-creditworthiness of the borrowers. For the most part, the “flippers” and other borrowers MOR Financial scopes have great credit. In the past, hard money lending was often seen as the realm of the hard-luck borrower. Mehra suspects, “Maybe 20 years ago, that was the case, but a lot has changed. Banking guidelines being as stringent as they are have really opened things up for private money lending. Where else are people supposed to go to get the access to leverage?”

Morsi adds, “Today’s investors are strong and hungry.” Since MOR comes from the customary lending side, the company strives to maintain and deliver on customer service. And deliver they did. MOR Financial has set themselves apart by taking the insight of due diligence and recalibrating it in a way to center on becoming trusted advocates for their borrowers.

“We always try to play the devil’s advocate for their benefit,” said Mehra. “Not to kill the deal, but to make sure our affiliates aren’t walking into a black hole.

As the company’s directors, Sean and Ajay look at every deal as though it was their own so they can provide bona fide feedback to their clientele.

With repeat borrowers, MOR has rapport in the industry. The company aims to educate everyone from their able borrowers to individuals just breaking in — and they work with a lot of beginners.”

“We’ve always felt that the most durable relationships are built through education,” mentioned Mehra. Since MOR has considerable professional relationships with their borrowers, it brings perhaps an unexpected benefit: fewer defaults.

Mehra and Morsi both feel strongly on not being viewed as a corporation, but as a part of a business network working conjunctively to meet each other’s needs. Out of 360 plus transactions that they’ve written, only two notices of default have occurred.

Mehra and Morsi both feel strongly on not being viewed as a corporation, but as a part of a business network working conjunctively to meet each other’s needs. Out of 360 plus transactions that they’ve written, only two notices of default have occurred.

One of MOR Financial’s core principals centers on the belief of education and the conventional techniques of equity partnership arrangement, mainly structured for borrowers who are just starting out.

“You can literally walk into a deal with no cash out of your pocket,” said Morsi. “We’ll provide the investors willing to bring capital to close and supply the rehab funds. All you need to have is a great asset and an ability to manage a property. The financing side we’ll take care of.”

The program has allowed many of MOR Financial’s clients to evolve. With their eminent skill and market presence, they’ve won over the masses. Clients effortlessly transform from wholesaling a deal to doing their first flip. MOR Financial is giving beginners an opportunity that cannot be captured elsewhere.

For information about MOR Financial visit wwwMORFinancial.com

For information about MOR Financial visit wwwMORFinancial.com

{kind=link}